What is the difference between secured debts and unsecured debts when you declare bankruptcy in Canada? Bankruptcy is a chance to start over, and while it does eliminate most debts, it does not deal with them all. One of the biggest distinctions when filing bankruptcy is whether or not your debt is secured or unsecured.

Click to view full infographic

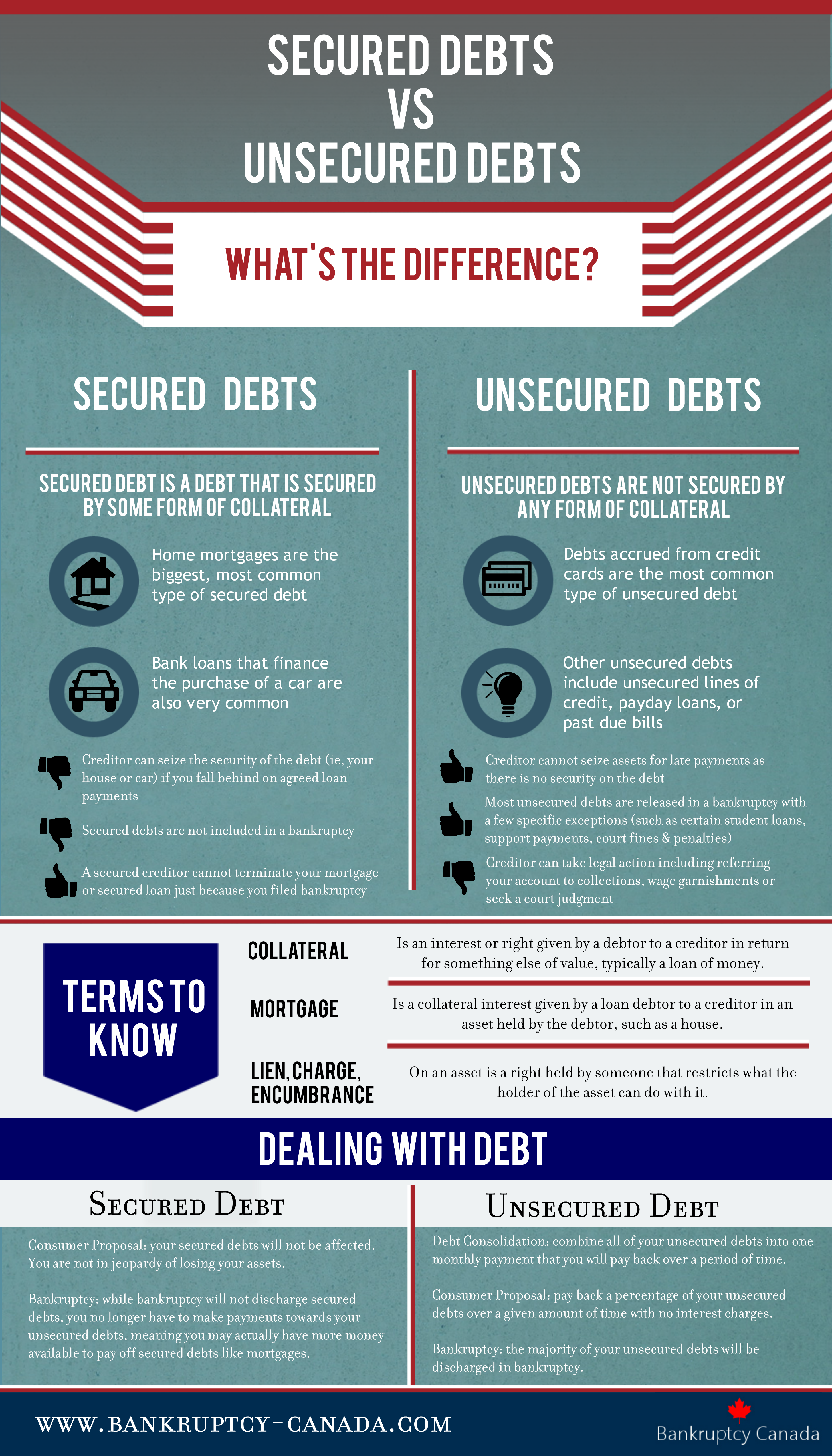

Secured Debt

What is a secured debt?

Secured debt is a debt that is guaranteed by having assigned some form of collateral. In the event of non-payment, a secured creditor can begin proceedings to seize the security you have pledged against the loan. Some common examples are house mortgages and secured car loans however almost any loan can be secured including lines of credit and bank loans. Even a credit card can be secured. A secured credit card is often used after filing bankruptcy to help you rebuild your credit.

Secured debt can be created when you take out a loan (such as a mortgage) but can also be created by creditor action such as a lien, charge or other encumbrance placed on an asset you own (such as a tax lien on you home).

Secured Debt and Bankruptcy

The important thing to know is that secured debts are not included in a bankruptcy. If you own a home and file bankruptcy, assuming there is no equity in the home, you can continue to make your mortgage payments and live in your house. Also, a secured creditor cannot terminate your mortgage or secured loan just because you filed for bankruptcy in Canada.

While bankruptcy does not discharge your secured debts, the fact that you no longer have to make payments towards you unsecured debts means you may have additional cash flow available each month to pay your mortgage or car loan, reducing the risk that you will lose those assets.

In the event that you have equity in any asset that is secured by a mortgage or other debt, a consumer proposal is a great option that allows you to keep that asset.

Unsecured Debt

What debts are unsecured?

In contrast, unsecured debts are not secured by any form of collateral, asset or guarantee. The most common types of unsecured debts are credit card debt, unsecured lines of credit, payday loans and past due bills.

Since you have not pledged any assets against these debts, creditors cannot seize anything for non-payment. Creditors can however still take action against you if your payments are in arrears including sending your account to collections or pursuing a wage garnishment.

Unsecured Debts and Bankruptcy

If you have significant unsecured debt, a bankruptcy will eliminate most unsecured debt with only a few exceptions such as certain student loans in bankruptcy, support payments, court fines and penalties. A consumer proposal allows you to pay back a percentage of what you owe over a period of time with no interest.

To better understand how your unsecured or secured debt will be handled in a bankruptcy or a consumer proposal, talk to a bankruptcy trustee in Canada about your options.

Hi. Thinking Capital is saying they are going to sue me for an unsecured loan of $39,000 I owe because I was forced to close a store. I am in the process of filing personal bankruptcy. The only asset I have is a home with very little equity. Can they make me sell my home and garnish any future wages ?

Hi Laura. If you file bankruptcy, an unsecured creditor cannot force you to sell your home. How your home will be handled in bankruptcy will depend on the amount of equity you have. I suggest you discuss this with a licensed insolvency trustee who can give you a specific answer for your unique situation.

Hello – I really need your advice….

I had stage 3B cancer in 2012, had to leave my job. Spent over a year battling it with chemo/recovery. I had to get disability benefits. During this time my employer hired two people to cover my job – when I returned I didn’t have enough hours to pay rent/expense, and my back was injured and restricted my abiity to earn. Stark choice – I had to keep the disability benefit to live or I would literally have been out on the street. I tried to get other work but was unsuccessful, and my back issues intensified to the point where I had to leave work in 2018 as I could no longer perform my duties. Tried to find other work, was unsuccessful. In 2020 the gov’t stopped the payments, said it was an overpayment and told me I had to pay it back – $42,176. Insane. I’m 62, with Pirifiormis Syndrome back injury and chronic pain, due to Covid I have no job, surviving on the CERB and am living in subsidized housing. I told the gov’t all this AT LEAST TWICE, but they don’t seem to care. Help! What are my options?

Appeal the government decision to disallow your benefits. If that is unsuccessful then you’ll need to find an advocate (lawyer) to plead your case. If the government takes the position that you were not eligible for the benefits you received then the debt may not be dischargeable by bankruptcy. As a stop gap measure, at 62 you may apply for CPP, but the government may deduct something every month from the benefit to recover the overpayment. Sorry.

Hi.I am under consumer proposal.My trustee made a mistake.He filed my secured home equity line of credit as unsecured.first of all, when I filed the trustee did not explain the difference of secured from unsecured.is that the reason why I am paying much?I have 36k home equity line.maybe that affected the calculations of how much I owe .would there be a difference if my trustee did the correct filing ?I am just wondering if my trustee filed my home equity in the secured, i might pay less? thank you

This is a conversation you should have with your trustee. If you are not satisfied with their answers then perhaps you should speak to the Office of the Superintendent of Bankruptcy. When you provide your trustee with a list of who you owe at the start of a proposal you have to tell them if a debt is secured against you house. If you did not do that it is likely the trustee treated the debt as unsecured and it may have impacted your payments. You have the right to AMEND a proposal (which means have it changed) after it has been accepted by your creditors. Your trustee needs to send out a new information package that explains what has changed (the secured line of credit) and what the new proposal terms are going to be. Your creditors then get to vote all over again on the new deal. If you offer the same rate of return they should agree, but this is something you have to discuss in detail with your trustee.

Hello – I really need your advice…

After a TRAIL of divorce matter a court order stated, that the ” Ex” owns me spousal obligations of fixed payment based on unjust enrichment. Immediately thereafter, the Ex” fabricated a fake Bankruptcy, where this debt was filed as unsecured. It is important to note, that his debts actually contain 98 % from the total of all creditors. My question is:

1. is spousal obligations an object for Bankruptcy in my case?

2. is spousal obligations in my case, “unsecured” or “secured” creditor?

3. if exist in Ontario some Law, how I could trace this debt to me (spousal obligations) and which steps I should proceed with that?

4. how long after Bankruptcy I would have some rights to ask for these debts?

Thank you in advance

Respectfully

Marina

Sorry, but you need to speak to a Family Law lawyer, not a bankruptcy trustee. Support payments cannot be eliminated in a bankruptcy. Asset equalization payments can be. If a Court Order was based on “unjust enrichment” then it may fall under the “debts not dischargeable rules in Section 178 of the Bankruptcy and Insolvency Act. Certainly worth a look… Keep in mind that there are things you can do during your ex’s bankruptcy, particularly if you represent he majority of the debt. Again, something to discuss with your lawyer.

Hi,

I owe money for parking tickets. Can the city issue me tickets if I file a consumer proposal or bankruptcy? Can they still lien my car? Wondering how fines are dealt with and to whom their fines are sent to?

Hi Aliza. Yes, the city can still issue tickets. Government fines are generally not discharged in a consumer proposal or bankruptcy. Your licensed insolvency trustee can review the tickets and give you a more complete answer given your specific situation.