It’s an interesting dilemma. You owe money to creditors but don’t have enough money to keep up with the payments. You are on a limited income and don’t even know if you have enough money to file for bankruptcy. In those circumstances what can you do? Is a do nothing strategy a better alternative, at least for the time being, than declaring bankruptcy?

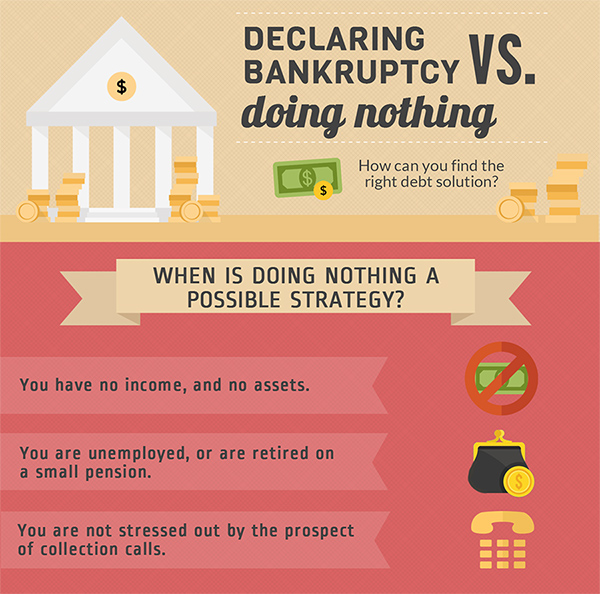

When Is Doing Nothing A Possible Strategy?

The purpose of declaring bankruptcy is to eliminate your debt so that creditors stop calling. However if you have no ability to pay your creditors, you may be what they call ‘creditor proof‘. This means although you may receive requests for payment, there is little opportunity for creditors to pursue you other than to keep asking for payment.

When does it make sense to tell you creditors you can’t pay and just ignore them?

Click for full infographic

{kind=link}

You have no income and no assets. Your creditors will not be able to garnish your wages, because you have none. You may be unemployed, or retired on a small pension. Creditors cannot easily garnish pension income.

There is one large caveat to this strategy however. You must be able to tolerate the potential for constant phone calls from your creditors and collection agencies. They are likely to continue to call to see if there is a change in your circumstances or to see if they can wear you down and at least receive some form of payment.

There are options to stopping the calls. Declare bankruptcy anyway, although you will need to be able to afford the monthly payments. Or you can offer to settle with your creditors, telling them you have no income and no likelihood of any income in the future. They may be willing to accept a small partial payment as settlement of your debt.

The Consequences of Doing Nothing

There are consequences to choosing to hold out against your creditors rather than file bankruptcy. As we noted above, your creditors are likely to continue to call. Once you return to work they may begin proceedings to garnish your wages.

It’s also important to note that your credit card and other debts won’t just go away. It can take years to pay off debt when all you are doing is making the monthly minimum payments. And if you are in arrears, you may never catch up.

If you choose a do nothing strategy and stop making payments on your home, car or other secured loans, you can expect your creditors to pursue every avenue they have to collect. This will include repossession and foreclosure. Even without an income, bankruptcy can help you deal with these consequences if you have some income available to make the required monthly payments for 9 months (assuming this is your first bankruptcy).

Temporary Resolution

Sometimes the do nothing strategy is a good temporary resolution. This is the strategy you choose while you continue to look for work or until your situation changes. The best approach would be to advice your creditors you have no income and cannot make payments. Once you do return to work, contact a bankruptcy trustee to discuss your options to deal with the accumulated debt so that you can return to work knowing your financial situation will improve in more ways than one.

Leave A Comment